By ETimes

Financial Performance Highlights

- Listed property concern Mashonaland Holdings posted a ZWL$17.2 billion after tax profit for its financial year ended 31 December 2022. The performance represented a 458% inflation adjusted rise from comparative 15 month period ended 31 December 2021.

- The sharp rise in profits was supported by fair value gains of ZWL$18.7 billion to the groups investment properties. Operating profit before fair value gains increased by 243% to ZWL$3.5 billion.

- Revenues increased by 98% to ZWL$3.8 billion with revenues from the Mashview Gardens cluster contributing 30% at ZWL$1.2 billion. Rental income amounted to ZWL$2.6 billion which was attributed to periodic rental reviews and occupancy levels increasing from 81% to 87%.

- The group generated net operating cash flows of ZWL$1.1 billion while the disposal of the Charter House property generated a positive net investment expenditure of ZWL$1.4 billion and a positive overall net cash flow of ZWL$3 billion.

- During the period the group acquired a 4ha site in Pomona for the development of a wholesale center. Construction is expected to comment in April 2023 and 85% envisaged facility has already been pre-leased.

- The group also acquired a 2ha site along Borrowdale Road for the construction of an office park. Construction on the project is expected to commence in the second quarter of 2024.

- The 1st phase of the Mashview Gardens cluster housing project was completed and all 25 units were pre-sold during the period. Phases 2 and 3 are expected to be completed in second quarter of 2023.

- Construction works are proceeding at the Milton Park Day Hospital Project and is expected to be completed in August 2023.

- At the end of the period the groups Total Assets stood at ZWL$73.2 billion, with investment properties making up ZWL$66.9 billion and cash holdings adding ZWL$4.1 billion. Total liabilities reached ZWL$7 billion, with borrowings of ZWL$2 billion and payables of ZWL$1.6 billion.

- Looking ahead, the group noted its strategic focus of portfolio diversification and increased operational efficiencies. The group also noted risks that may undermine short term economic recovery in the resurgence of COVID-19 infections, the potential global supply-chain disruptions, geopolitical tensions in Europe and the upcoming local harmonized elections.

- The group declared a final dividend of ZWL$212 million, with a component of US$200,000 to be paid in foreign currency.

Commentary and Analysis

Zimbabwe’s real estate sector has drawn increasing attention as local investors look for safety against inflation risk or a secure store of excess cash outside the local banking system. Perhaps it is fitting that Mashonaland rebounded so sharply to profitability during the period. Although fair value gains contributed significantly to the upturn in the bottomline, analysis suggests the revenue earned during the year set a seven year high. Evidently, the group was been able to exploit the demand for property investments with the Mashview cluster project, which contributed which accounted for 30% of the revenue earned. The disposal of the Charter House added to groups internally generated cash flows to leave it sitting on healthy cash balance of ZWL$4.1 billion.

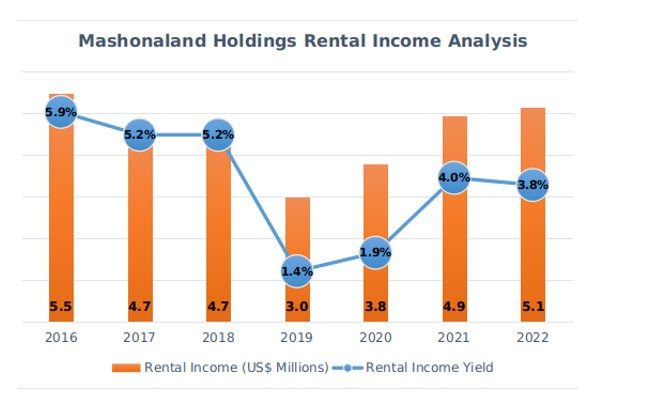

So overall, it looks like Mashonaland Holdings is in relatively sound financial shape. High borrowing costs are likely to restrict the group to relying primarily on internally generated funds to complete its marquee pipeline projects (Borrowdale Rd office park and Pomona wholesale center) which is likely to drag completion times. Perhaps underlining the importance of the projects, analysis suggests the rental income from the groups present portfolio has been subdued, with rental income yields still moderately below the dollarized era levels despite some recent improvement. So, expectations are for the short-term focus to be on continuing to exploit the investor appetite for real estate with more cluster housing projects. The long-term viability and sustainability of the demand is debatable, but Mashonaland has a reputable brand that could be leveraged for small, fast turnover high quality projects as suggested by the Mashview project.

On the ZSE, the Mash Holdings share is currently trading at ZWLc1,325, with a real YTD return of 3% and a price to book ratio of 0.3x. Recent market developments have seen financial group ZB Holdings take up a controlling stake of 50.5893% in the property company. Given Mash Holdings’ significant cash balances, relatively low gearing and high cash flow generation capacity, at ZWLc800 per share the deal looks like a bargain for ZB – Harare

Advertisement

Discover more from Etimes

Subscribe to get the latest posts sent to your email.