Loyalty miles have quietly become one of the world’s most sophisticated financial instruments. For Southern Africa, the real lesson is only just beginning.

By Jabulani Simplisio Chibaya

HARARE – THERE is a moment, somewhere over the Atlantic at 35,000 feet, when you might sip a complimentary drink and think the airline is rewarding your loyalty. You would be partially right. But you would also be missing something far more interesting — and far more instructive for every business operating in Africa today.

Airlines long ago stopped being primarily in the business of flying people. They are, in the most precise financial sense, banks that happen to own jets. And the currency they print — frequent flyer miles — has become one of the most ingeniously engineered financial instruments of the modern era. Understanding how they did it is a masterclass in data, human psychology, secondary markets, and the architecture of money itself.

KEY FIGURES

$6.4B Delta loyalty revenue, 2023

$5.5B Delta operating income, same year

~$1T Est. unredeemed miles globally

THE HIDDEN BALANCE SHEET

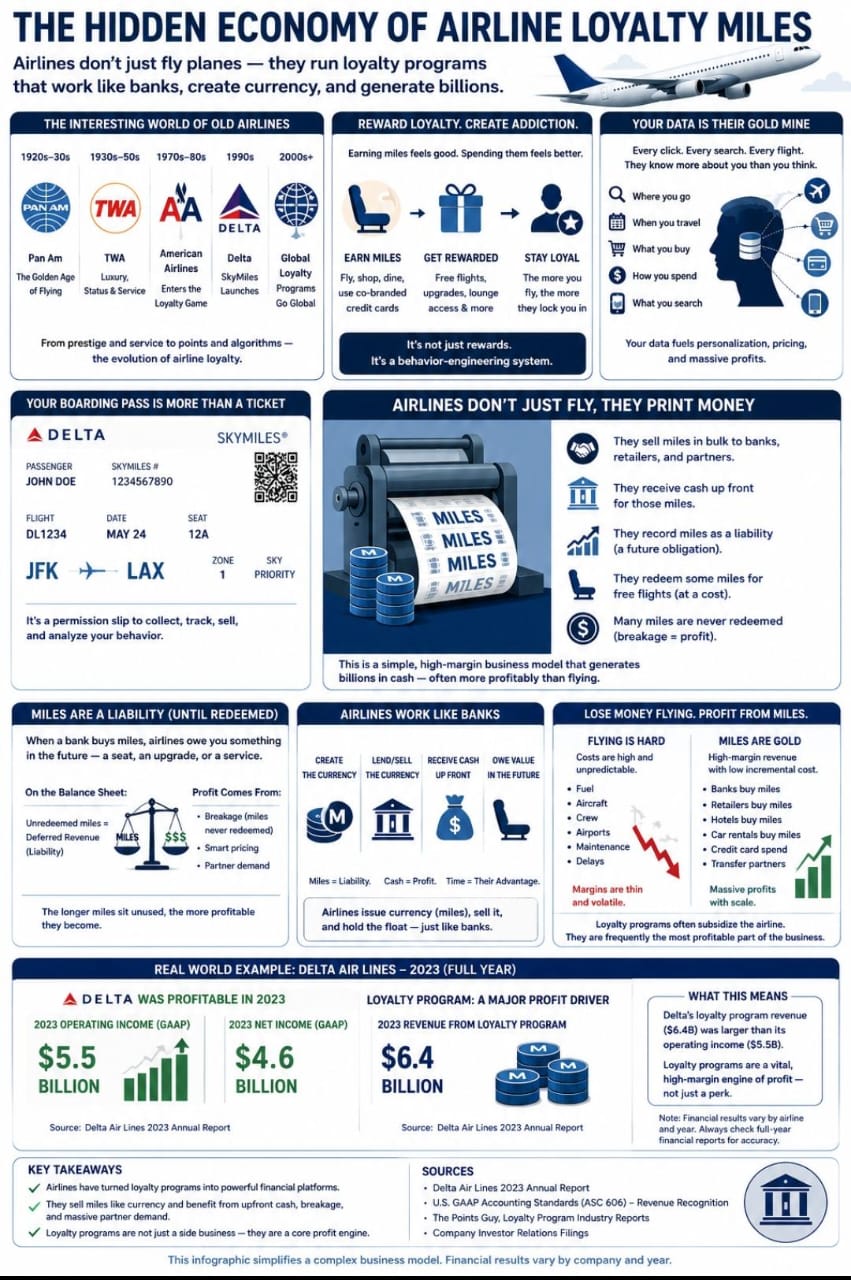

In 2023, Delta Air Lines reported $5.5 billion in operating income. Impressive for any company. But buried within that annual report was something that quietly rewrites the story: its SkyMiles loyalty program generated $6.4 billion in revenue. The loyalty program, in isolation, outearned the airline’s entire operating business. The jets — those enormous, fuel-hungry, weather-delayed, maintenance-intensive machines — were, in a sense, the marketing department for a financial services operation.

How? Airlines sell miles in bulk to banks, credit card companies, hotels, and retailers — collecting cash upfront. Those miles then sit on the balance sheet as a liability: a future obligation. But here is the beautiful asymmetry at the heart of the model. Every mile that is never redeemed — through expiry, disinterest, or complexity — converts from liability to pure profit. The system is engineered so that a meaningful percentage of the currency it creates simply vanishes. In banking terms, this is known as breakage. In airline terms, it is a business model.

“Miles are a liability until redeemed — and the longer they sit, the more profitable they become. It is a financial instrument disguised as a thank-you note.”

PRINT MILES → SELL TO BANKS → RECEIVE CASH FLOAT → BREAKAGE = PROFIT

DATA IS THE REAL PRODUCT

But miles are only half the story. Every search, every booking, every seat preference, every meal choice, every connection airport and layover duration — all of it is data. And airlines have spent decades building infrastructure to collect, store, and monetize that data in ways most passengers have never imagined. Your boarding pass is not just a permission to fly. It is a permission slip for the airline to track, profile, and act on your behaviour.

This is not conspiracy — it is disclosed, agreed to, and enormously profitable. Airlines know where you go, when you travel, what you buy mid-flight, how you respond to upgrade offers, and how price-sensitive you are on any given route on any given day. This semantic richness — the meaning embedded in behavioural patterns — is what Tomasz Tunguz described in Winning with Data as the true competitive moat of data-native businesses.

Carl Anderson’s work on data-driven organisations makes the point even more starkly: companies that treat data as infrastructure — not as a byproduct — consistently outperform those that treat it as a reporting tool. Airlines have operationalised this. Every price you see on a booking page is the output of a machine learning model trained on billions of historical transactions and real-time demand signals. You are not seeing a price. You are being shown the price the algorithm has calculated you are most likely to pay.

CLOSER HOME: THE SIMBISA LESSON

CASE STUDY · ZIMBABWE

Simbisa Brands — Zimbabwe’s largest quick-service restaurant operator — launched a loyalty rewards program that customers rapidly began using as an informal money transfer mechanism. The regulators noticed. Simbisa was eventually required to acquire a microfinance licence. What started as a marketing tool had, through customer behaviour, evolved into financial infrastructure. The customers built the product the business hadn’t planned.

This is perhaps the most important lesson for entrepreneurs and business leaders across Southern Africa: products are not defined by their creators — they are defined by the problems they solve and the behaviours they enable. Simbisa did not set out to build a money transfer service. Its customers did that for them, and the regulators confirmed it by requiring the appropriate licensing.

This is precisely where Austrian economic thinking offers a compelling lens. Friedrich Hayek’s insight that knowledge is dispersed — that no central planner can aggregate the real preferences of real people better than a functioning market — applies directly here. The customers who used Simbisa’s points as currency were expressing genuine demand for a service that no bank or mobile money provider was adequately offering. The loyalty program, inadvertently, discovered a market gap.

THE UNTAPPED FRONTIER: AFRICAN AVIATION AND ADJACENCY

Now consider what African airlines could do if they approached this deliberately. The continent’s aviation sector carries roughly 100 million passengers annually — a number growing faster than any other region. Yet the sophisticated secondary revenue architecture that Delta, American, and United have built over decades is largely absent from African carriers. Most African airlines earn the overwhelming majority of their revenue from selling seats. They are flying planes and calling it a business, when the real business — the data business, the currency business, the financial services business — remains almost entirely unexploited.

An African airline with the right ambition could partner with mobile money operators — M-Pesa, EcoCash, MTN Mobile Money — to issue miles that double as digital wallet credits. It could sell miles in bulk to regional banks, microfinance institutions, and fast-moving consumer goods companies eager for a loyalty layer. It could use its flight data — who travels between Harare and Johannesburg, how often, on what budget — to build credit profiles for the unbanked. A passenger who flies four times a year has demonstrated income, mobility, and planning capacity. That is a credit profile. That is bankable data.

“The passenger is not the product. The passenger’s pattern is the product. And in Africa, those patterns are almost entirely unmined.”

CROSS-INDUSTRY CONVERGENCE: THE REAL OPPORTUNITY

The framework extends far beyond aviation. Insurance companies sitting on decades of claims data are only beginning to understand what that data is worth in dynamic pricing models. Pension funds managing long-horizon assets have almost no real-time insight into the economic behaviour of their beneficiaries. Asset managers in markets like Zimbabwe operate in information-sparse environments where even basic signals — consumer spending, mobility patterns, sector growth — are difficult to price.

Meanwhile, payment processors and buy-now-pay-later operators are generating transaction-level data that is extraordinarily rich. Every split payment, every deferred purchase, every repayment pattern is a signal. In mature markets, this data is being used to underwrite credit at a granularity that traditional scoring models cannot approach. In Southern Africa, most of this data is collected, stored, and left to age in servers that are never interrogated for insight.

The question for any financial services player in the region is not whether to collect data — they already do — but whether they are building the organisational muscle to act on it. And here the convergence of AI changes everything. Tools that required data science teams of dozens, server farms, and months of modelling can now be approximated with a fraction of that investment. The moat that kept small-market operators from competing with global firms on data sophistication is narrowing rapidly.

DESIGN THINKING MEETS FINANCIAL ENGINEERING

What African markets require — and what the airline loyalty model ultimately demonstrates — is the fusion of product thinking and financial engineering. The best loyalty programs were not designed by actuaries alone, nor by marketers alone. They emerged from a genuine understanding of human behaviour: that earning feels good, that spending rewards creates dopamine, that status tiers engineer aspiration, and that the fear of losing accumulated value drives retention more powerfully than any advertisement.

Zimbabwe’s small and interconnected economy is, paradoxically, an advantage here. Cross-functional collaboration — between telecoms, banks, retailers, airlines, and hospitality operators — is logistically easier than in sprawling markets. A frequent flyer program that integrates with a hotel chain in Victoria Falls, a supermarket group in Harare, and a mobile wallet across the region is not a complex technical lift. It is a coordination problem. And coordination problems are solvable when the incentives are aligned.

Tourism offers the most immediate entry point. Zimbabwe, Zambia, Botswana, and Mozambique collectively offer one of the world’s most distinctive tourism corridors. An integrated loyalty ecosystem linking air travel, lodge accommodation, safari operators, and local craft markets — with data flowing across all of them — would create consumer profiles of extraordinary depth. Those profiles are monetisable in ways that the current fragmented, cash-heavy, loyalty-free system simply cannot access.

DATA AS INFRASTRUCTURE: THE AI ACCELERANT

Perhaps the deepest insight from the airline loyalty story is this: data is now infrastructure. Not a byproduct, not a report, not a compliance obligation — infrastructure, in the same category as roads, electricity, and bandwidth. The businesses that will define the next decade in African commerce are those that treat their data infrastructure with the same seriousness they treat their physical infrastructure.

AI is the accelerant. The ability to find patterns in large, messy, heterogeneous datasets — the kind that African businesses generate daily — is now accessible to organisations that could not have afforded it five years ago. The airline that knows, with statistical confidence, which of its loyalty members are likely to churn in the next ninety days can intervene with a targeted offer before that churn happens. The insurance company that can identify early signals of financial stress in its policyholders can adjust premiums, offer products, and retain customers before a competitor does.

The miles economy is a masterclass in all of this. It is a hedging strategy, a financial instrument, a data collection mechanism, a behavioural engineering system, and a brand loyalty tool — all wrapped in the emotionally satisfying package of a free flight upgrade. African businesses do not need to copy it directly. They need to understand its principles: find the secondary value in what you already collect, engineer the incentives that change behaviour in your favour, and build the data infrastructure that makes the whole system compound over time.

The planes will keep flying. The question is who is building the bank behind them.

Sources: Delta Air Lines 2023 Annual Report · The Points Guy · Tomasz Tunguz, Winning with Data · Carl Anderson, Creating a Data-Driven Organisation

Jabulani Simplisio Chibaya is a Data and AI Consultant specializing in data science, artificial intelligence, blockchain, and cryptocurrency innovation. A seasoned conference speaker, he also writes on the intersection of technology, regulation, and economic development. Contact: Cell: +263 778 921 881, Email: simplisiochibaya22@gmail.com, LinkedIn: https://www.linkedin.com/in/jabulani-simplisio-chibaya

Discover more from Etimes

Subscribe to get the latest posts sent to your email.